Convio (Nasdaq: CNVO $10.60) is a leading provider of solutions for nonprofit organizations (NPOs). The company helps organizations more effectively raise funds and form relationships with donors, activists, volunteers and other constituents. Convio does the bulk of its work online, and can adapt an organization’s offline materials onto computers. Customers raised $1.3 billion in 2010 using Convio’s products, and 4 billion e-mails were delivered to over 140 million people. Nonprofit organizations used the company’s technology to fuel over 32.5 million advocacy actions to state and federal elected officials and other targets of cause-related campaigns.

The company’s products include the Convio Online Marketing platform (COM) and Common Ground, a constituent relationship management application. Convio Online Marketing helps an organization get the most out of advertising its advocacy on the internet by targeting constituents through e-mail and social media. Common Ground organizes NPO data from both online and offline sources so the info can be consolidated in a central location for NPO workers to easily access.

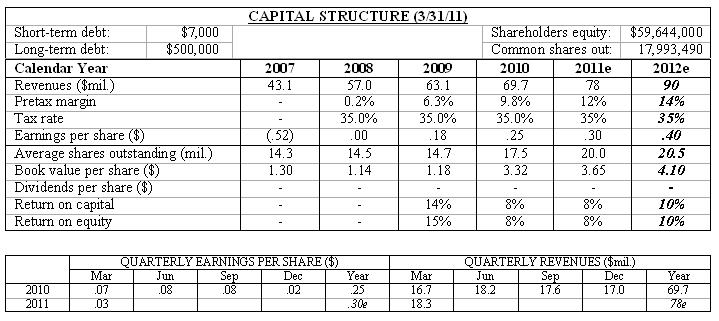

Revenue grew to $69.7m in 2010, up from $21.5m in 2006, but only increased 10% from 2009 ($63.1m). We estimate revenues will rise again to $78m in 2011 and continue to $90m in 2012. Most of the company’s revenue comes from sales; they also receive a percentage of funds raised for special events like charity runs or rides organized using Convio software. StrategicOne, LLC was acquired in January as Convio attempts to further penetrate the large- and enterprise-size NPOs. StrategicOne specializes in data management, which has helped Convio to optimize Common Ground.

The slow increase in revenues can be attributed to (you guessed it) the slow economy. Not-for-profits account for about 2% of the U.S. GDP, which is noteworthy but certainly not substantial – if Americans had less disposable income to spend charitable donations would likely fall off.

Revenues appear smaller due to the company’s accounting technique. Customers buy software and services from Convio on 1-4 year contracts depending on the service. Customers can opt to cancel the contract after a certain amount of time, so revenue from new contracts is initially only reported so far as the contract is guaranteed. Contract fulfillment isn’t a problem, as more than 90% of existing customers are retained with new plans.

The company’s stock price is high in relation to earnings per share at $10.60. Share earnings were $.25 in 2010 and project to $.30 in 2011 and $.40 the next year. Convio reported a 9.8% pretax margin in 2010, and that also should continue to rise to 20% over the next 3-5 years. It’s too early to suggest the company now, but we’ll keep a close eye on it and it could become a good earner in the future.

Convio has a strong business model and no true competitor. Blackbaud also assists NPOs; that company has higher revenue and a larger built-in-base, but its services are more traditional (hard mail, phone calls). Blackbaud is altering its business for the internet, but Convio has the upper hand as far as the Web goes.

The future looks promising for Convio. Revenues are rising, and could jump once the economy recovers. The company is also gaining respect among larger companies, so an acquisition is a possibility. Convio is located in Austin, TX.

( Click on Table to Enlarge )