Napco Security Systems (NSSC $3.00) is a leading provider of home security products, which are re-sold by distributors and local installation companies. The company has developed relationships with most of the industry's leading re-sellers. In the past the company focused primarily on standard access control and alarm systems. At the peak of the market in 2008 Napco purchased a leading lock manufacturer ("Marks"), which expanded its product line but saddled the company with debt obligations. Napco was able to keep its head above water while sales nosedived during the recession, helped by a low cost manufacturing base in the Dominican Republic. Well established relationships with major dealers like ADT enabled Napco to maintain pricing and market share, as well. The Dominican operation also provides for a reduced tax rate. Most of Napco's competitors retrenched during the downturn to conserve capital and wait for better days. The company took the opposite approach. Product development activities were accelerated. Marketing programs were broadened. The company now is launching a series of computer-based products that promise higher profit margins, broader customer adoption, and potential cross marketing opportunities.

A wireless communication device offers the greatest immediate potential. In the past most home security systems sent alarms to police and other monitoring stations using conventional telephone lines. A rising number of households don't have landlines any more. Napco recently introduced a wireless transmitter to fill the void. Those devices also make it impossible for thieves to cut the phone line before going in. Napco's system costs significantly less than competitive wireless offerings, providing attractive margins for its re-sellers. They also usually generate recurring revenue that is divided between Napco and the re-sellers. Unit volume has been doubling every quarter since the product line was launched last fall. A remote monitoring package holds equally large potential. That software enables customers to control their house from a cell phone, performing tasks like turning the heat up and down, managing the lights, and watching what's happening through a series of webcams. As more appliances become computerized that technology could become increasingly popular. A television advertising campaign featuring NCIS's character Timothy Magee (the geek) is reinforcing consumer demand.

Commercial demand is advancing, too. Napco integrated its fire and security systems into a single package to simplify installation and management. It also upgraded the locking systems obtained in the 2008 Marks acquisition. The expertise required of its commercial offerings is being transferred to Napco's consumer products in a systematic fashion, moreover, driving quality up and costs down.

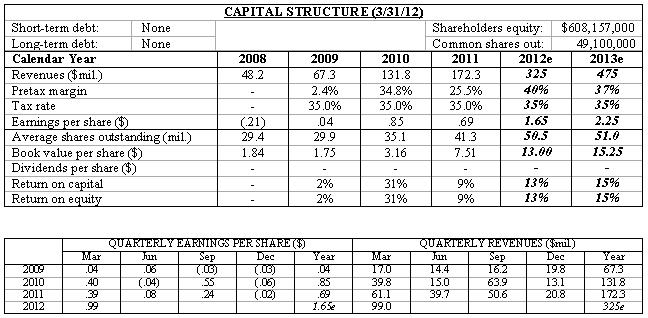

Earnings are on the upswing. We estimate non-GAAP income (which excludes acquired intangible amortization and stock option expense) will double in fiscal 2012 (June) to $.25 a share. Next year $.40 a share represents a realistic target. Margins promise to keep widening as volume climbs in subsequent periods. We estimate income will approach $1.00 a share within 2-3 years on sales of $100 million. Applying a P/E multiple of 15x to those earnings suggests a target price of $15 a share, potential appreciation of 400% from the current quote.

( Click on Table to Enlarge )