We're maintaining our (fully taxed) 2011 earnings estimate at $.25 a share. Ellie Mae is ramping up employment and infrastructure spending to separate itself from the pack even further. So even though mortgage volume might exceed industry forecasts this year all that spending probably will prevent margins from expanding much beyond our target. Significant leverage is possible in 2013. Average revenue per mortgage is likely to keep climbing. The number of deals per customer is likely to improve, as well, as users essentially throw away their fax machines and go entirely electronic. If the Government implements a mortgage re-write program further gains could be realized.

The housing industry remains at extremely depressed levels. Even if it never bounces back Ellie Mae promises to sustain above average growth by gaining market share, boosting revenue per transaction, and leveraging its fixed costs. If housing activity returns to normal substantial further gains are possible. A collaboration with Wells Fargo, which still is in early stage of development, could yield further impetus.

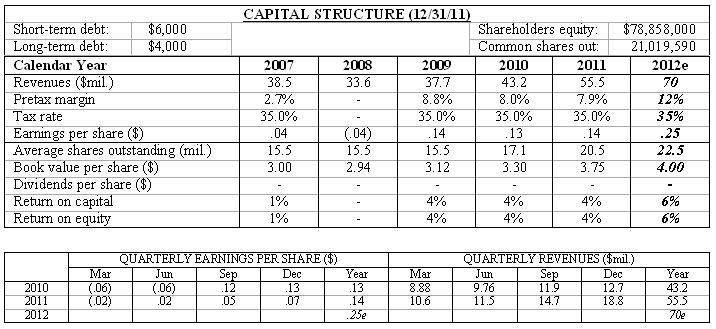

( Click on Table to Enlarge )

No comments:

Post a Comment