Several intellectual property acquisitions are in the pipeline. Acacia normally arranges a few large settlements at a modest discount when it obtains patents for its own account, to minimize risk. So further acquisitions could presage another near term revenue surge. Volume in the company's normal course of business also is climbing as patents obtained over the past few years -- both owned and partnered -- start to be enforced. It usually takes 1-2 years for Acacia to prepare a new portfolio for commercialization.

Large structured transactions could return to the scene, as well. In the past Acacia has licensed big chunks of its patent inventory in return for large one time payments. Last year when patent values escalated the company held off on making new deals for fear of underpricing them. Values now have stabilized, creating a greater likelihood of agreements being reached.

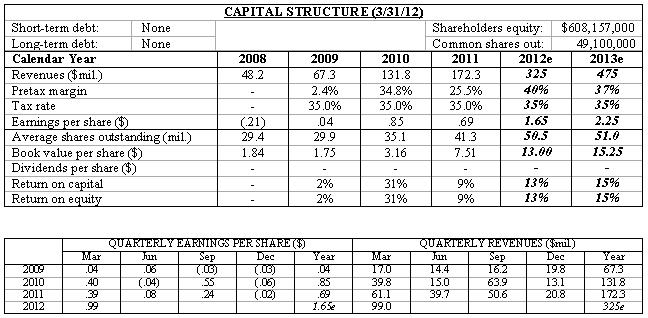

We are raising our 2012 earnings estimate by 10% to $1.65 a share. Next year $2.25 a share remains a realistic target. Acacia has penetrated only a small portion of its potential market to date. And that potential is likely to expand as more intellectual property is brought in house. In 2-3 years these shares could reach $100 a share.

( Click on Table to Enlarge )

No comments:

Post a Comment