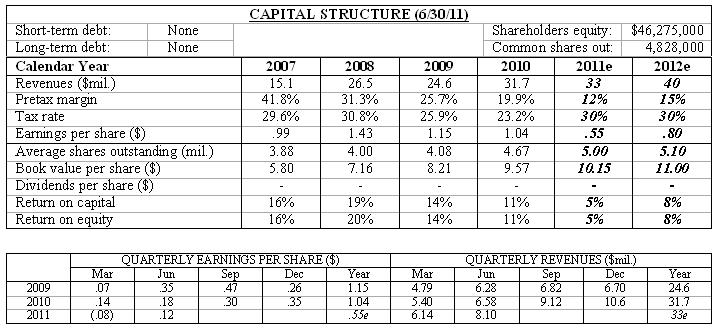

U.S. highway construction hasn't picked up as expected. In every recession since the automobile was invented government spending on transportation infrastructure expanded as a way to boost jobs while getting useful projects completed. When the Obama Administration took office in 2009 it touted expansive plans to invest in a plethora of "shovel ready" highway projects. The last three summers have seen little headway, though. Image Sensing has been facing macro-economic headwinds, as a result, amplifying its internal struggles. A near term improvement appears unlikely. We are reducing our 2011 full year earnings estimate 35% to $.55 a share, accordingly.

A new product, developed internally, could restore a bounce in the company's step. The line is aimed at Image Sensing's core intersection control market. It combines the company's machine vision and radar technologies into a single package to produce superior results at a reasonable price. With the error rate virtually eliminated competition should become less significant, helping margins. Attractive pricing also should help Image Sensing knock out indirect competition provided by loops that are buried under the roadway. Those systems are cheap but are expensive to install and repair.

The shares are unlikely to do much in the meantime. The new line is slated for introduction in Q1 of 2012. If Image Sensing can rehabilitate its foreign business during the interim performance could post dramatic gains next year. Value investors can realistically maintain positions with an eye towards tripling the stock price within 2-3 years.

( Click on Table to Enlarge )

No comments:

Post a Comment