Progress was achieved on the Moxie project. Argan is in line to engineer and build two natural gas fired electricity plants in the Marcellus Shale in Pennsylvania. The operating company, Moxie Energy, plans to fuel the systems with low cost natural gas from nearby fracking sites, eliminating the need to deliver it by pipeline. The electricity produced will be sold into the northeast market. Argan's potential revenue is in the $800-$900 million range. Final regulatory approvals and financing agreements are expected to be completed in the current quarter. Our fiscal 2014 (January) estimates assume only a modest contribution from the Moxie project. Work on the company's existing two projects will begin to wind down next year but the income generated should be sufficient to keep performance at a high level.

The Moxie build-out could support a much higher baseline of activity. That deal alone promises to lift revenues above current levels. Power generation in the U.S. remains below 2007 standards. But electricity consumption is rising, and the pace could accelerate if the overall economy improves. New facilities are likely use natural gas, solar, and wind power. Those are all Argan specialties. Tighter regulations on coal plants promise to reinforce the trend.

Argan is well positioned to succeed in what remains a competitive industry. The company's overhead is lower than larger participants. It also moves faster and fixes cost problems more quickly, minimizing over-run risk. Argan has added a lot of management and engineering talent over the past few years, though, allowing it handle complex jobs that smaller competitors have a hard time coping with. Assuming a modest inflow of new contracts in addition to the Moxie project, revenues could reach $500 million in 2-3 years to provide earnings of $3.25 a share.

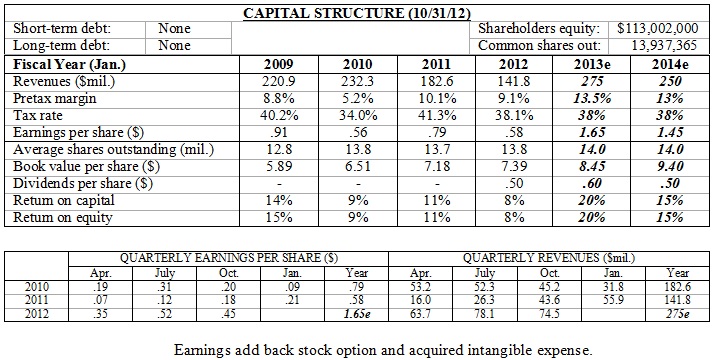

( Click on Table to Enlarge )

No comments:

Post a Comment